Ask an Expert

Ask an Expert

")

1. Executive Summary

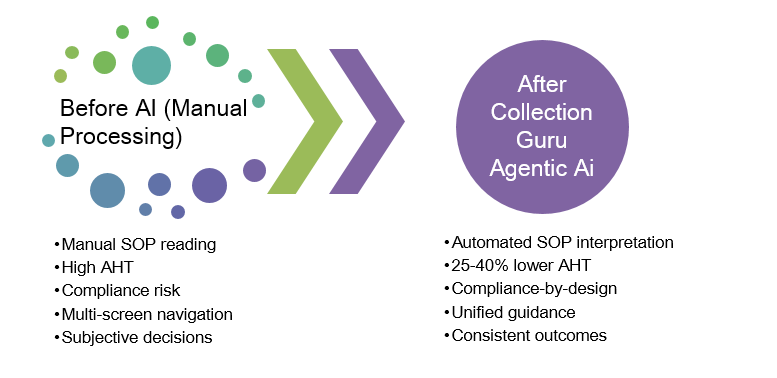

Financial institutions today face the perfect storm of rising arrears volumes, tighter FCA regulatory scrutiny, increasing operational complexity, and continuous pressure to deliver empathetic, consistent customer outcomes. Traditional approaches depend heavily on human advisors manually reviewing dense SOPs, navigating 20+ systems, executing FCA/CONC/MCOB-compliant procedures, and making subjective decisions—leading to inefficiency, inconsistency, and risk.

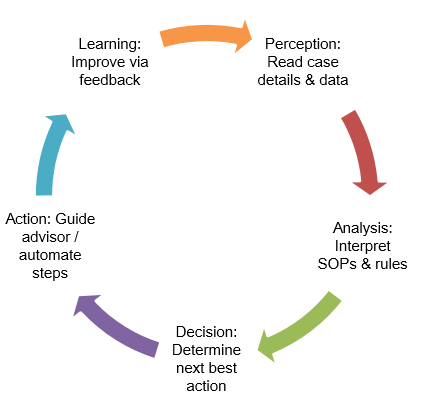

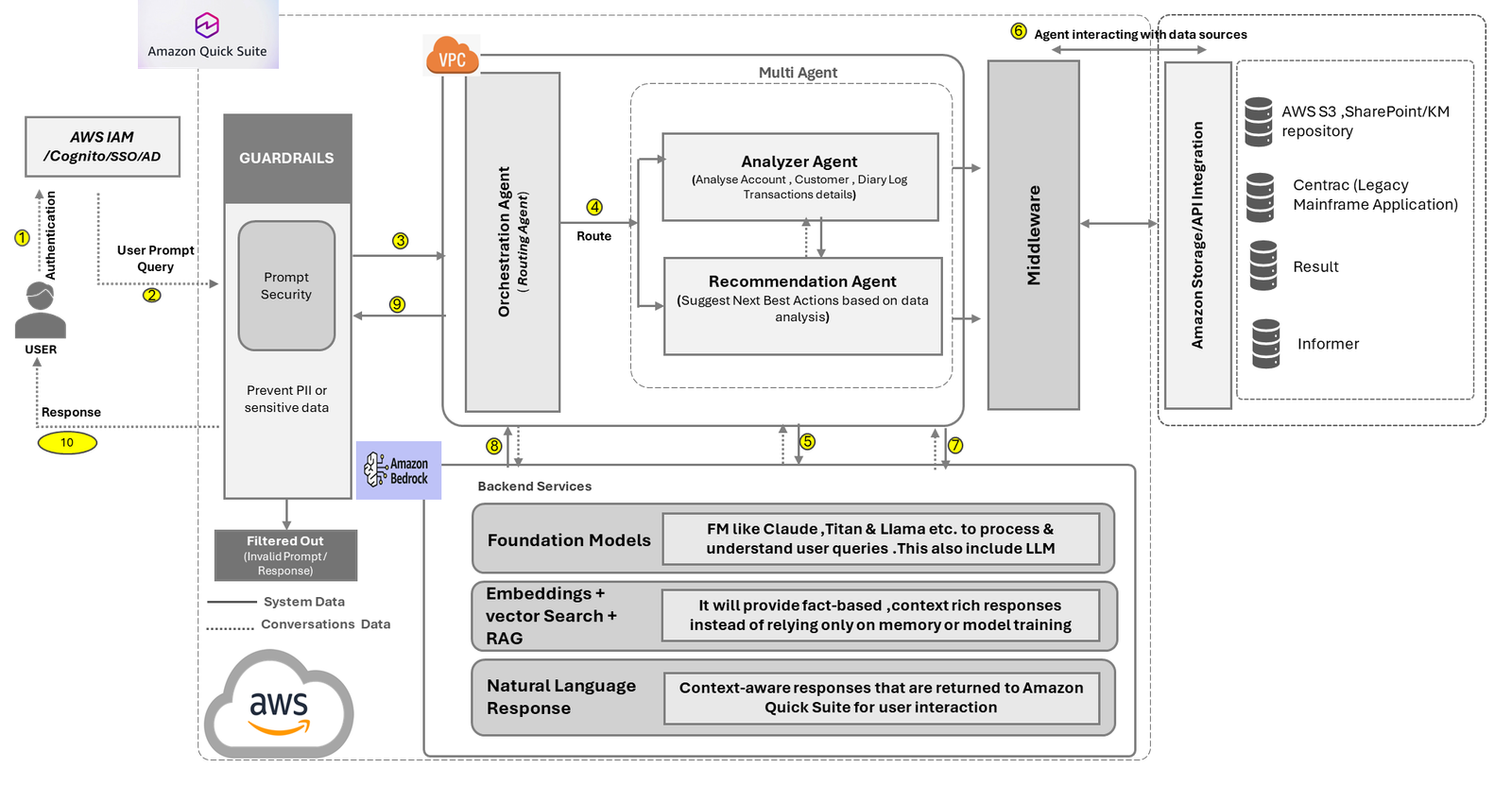

Collection Guru, an Agentic AI solution co-delivered with AWS, is designed to solve this industry-wide problem. The solution autonomously interprets operational manuals, applies rules, recommends next steps, generates compliant rationales, orchestrates multi-system workflows, and guides advisors in real time.

A large UK financial institution, Target UK, achieved:

- 25–40% reduction in Average Handling Time (AHT)

- ~40% reduction in manual effort & system toggling

- 60–95% accuracy in decisioning support

- Significant FTE optimisation & cost reduction

- Markedly improved compliance traceability and advisor confidence

This case study explains the problem, challenges, solution complexity, and the universal applicability of Collection Guru across regulated financial services.

Industry Problem: Why Debt Collection Is Harder Than Ever

2.1 Operational Complexity

Financial institutions must handle high-volume arrears cases daily, fragmented legacy systems (often 15–25 platforms), manual cross-referencing of detailed SOPs, multi-path call flows and decisions driven by root-cause analysis, affordability assessments, and forbearance logic.

2.2 Regulatory Burden (FCA / CONC / MCOB)

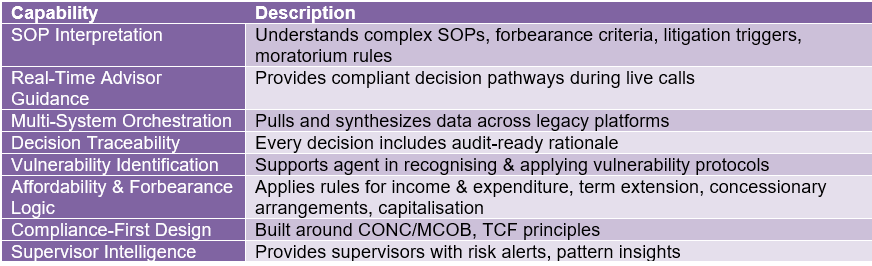

Institutions must demonstrate consistent, fair customer outcomes, they should apply or provide the right options: forbearance, breathing space, repayment arrangement, litigation decisioning, maintain auditability at every decision point and identify and treat vulnerable customers appropriately. It has to ensure compliance with CONC 7 and MCOB 13, including mandatory communications, pre-action protocols, and litigation-eligibility rules.

2.3 Advisor Burden

Advisors face cognitive overload interpreting multi-chapter operational manuals, subjective application of nuanced rules, stress of making high-stakes decisions in real time and frequent errors due to information scarcity and multi-system navigation.

2.4 Customer Expectations

Customers expect fast resolution, empathetic handling, clear guidance, transparent outcomes and reduced friction. Institutions struggle to deliver all these consistently through manual processes.

3. Core Challenges in Arrears Management Today

3.1 Manual SOP Interpretation

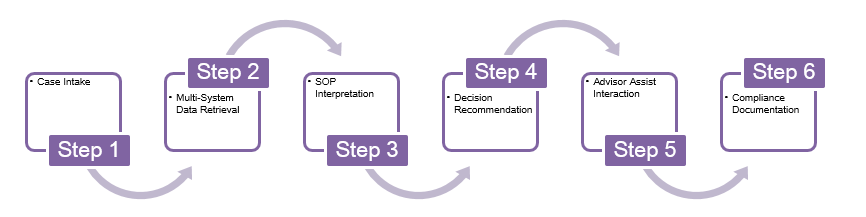

The Arrears Management Procedure Manual spans customer contact rules, affordability procedures, forbearance frameworks, litigious pathways, debt-solution frameworks (IVAs, DROs), vulnerability protocols, escalation & recovery processes and breathing space moratorium rules. Sometimes, advisors must interpret these rules in real time during a call—a near-impossible task.

3.2 Compliance Sensitivity

Each case demands strict adherence to contact windows, call-frequency rules, correct decision sequences, mandatory documentation, evidence-based rationales, suitability checks, forbearance criteria and litigation triggers & exceptions.

3.3 Variability in Decisioning

Subjective human judgement often results in inconsistent customer outcomes, risk of mis-treating vulnerable customers, misapplication of repayment plans, and poorly documented rationales affecting audits.

3.4 Lack of Unified Information View

Advisors toggle through Core banking systems, CRM, Payment history, Case notes, Manual calculators, & Policy documents this creates time loss, stress, and errors.

4. Why Traditional Automation Fails

Rule-based automation cannot handle multi-path case flows and ambiguous situations, here it needs interpretation of CONC/MCOB rules, human-like judgement, contextual understanding, exceptions & edge cases, parallel system orchestration & continuous compliance assurance. Debt collection is inherently cognitive, requiring contextual reasoning, not robotic automation. It involves multi-level planning and critical reasoning in order to execute an outcome via a strategy.